|

Policy rate cuts boosting stock prices: VinaCapital

The stock market recovery, which has been driven by lower interest rates in 2023, is likely to be sustained by higher earnings and attractive valuations in 2023, according to Michael Kokalari, chief economist at VinaCapital.

An investor watches electronic stock boards at a securities company. The 20 per cent surge in the VN-Index for the year as of August 8 has been largely driven by a circa 150bp fall in banks deposit rates. — VNA/VNS Illustrative Photo

|

In a recent note, he said the State Bank of Vietnam had cut policy interest rates four times this year -- the refinancing rate by 150 basis points to 4.5 per cent -- in stark contrast to its US counterpart, which has hiked rates four times, by 100bps to 5.5 per cent.

It also took other measures to boost growth, which fell to just 3.7 per cent in the first half of this year from 6.4 per cent a year earlier.

These policy rate cuts prompted banks to lower their deposit and lending rates, which helped boost the VN-Index by over 20 per cent for the year as of August 8.

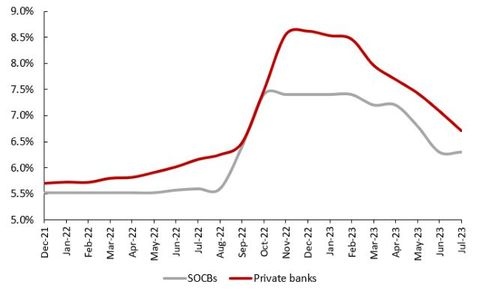

Chart shows average 12-month deposit rates at State-owned and private banks in Việt Nam. Lower interest rates this year have helped drive up stock prices. — Source VinaCapital

|

“We expect a sharp recovery in both GDP growth and earnings growth next year to propel stock prices even higher. That said, we do not expect the SBV’s monetary easing will have much of an impact on 2023 GDP growth because banks are currently hesitant to extend loans, and because higher interest rates are not the main source of Việt Nam’s slow economy this year.”

The aggressive policy rate cuts come at a time when the US and the EU are still raising interest rates.

A widening gap between interest rates in Việt Nam and in the US has put some depreciation pressure on the USD-VND exchange rate, but that depreciation pressure has been mitigated by a stunning improvement in the country’s trade surplus from zero in 2022 to 6 per cent of GDP in 2023, according to the economist.

This surplus, coupled with FDI inflows of over 4 per cent of GDP in the first seven months, helped support the đồng, enabling the SBV to cut interest rates while maintaining a remarkably stable exchange rate.

Impact of lower rates on stock, property markets

The VN-Index is up because people have been taking money out of banks and ploughing it into the stock market as their six-month deposits mature and because the market was oversold last year.

The increase has been driven by a 30 per cent surge in bank share prices and a 20 per cent increase in the prices of real estate stocks.

The heavy weighting of these sectors in the VN-Index (at 35 per cent and 18 per cent respectively) means the increase in their share prices drove over two-thirds of the increase in the index.

“The improvement in sentiment towards bank share prices stems from investors’ reduced concerns about asset quality issues and expectations for higher credit growth in H2, prompted by lower interest rates," the economist said.

“But it is important to note that declines in lending rates by banks are not uniform, especially given the liquidity issues mentioned above, which are particularly acute at some smaller banks.”

Lower interest rates boosted sentiment in the real estate market, where transactions are starting to pick up again, partly because mortgage rates dropped by more than 50bps at many banks over the last month.

“We expect another 50-100bp decline in mortgage rates over the next six to 12 months and note that the improved sentiment in the real estate market has, not surprisingly, boosted the sentiment towards major real estate stocks as well as towards the beneficiaries of higher real estate development activity (construction companies, steel companies, etc.).

“Finally, we expect a sharp pick-up in earnings growth in 2024, which means that the stock market recovery, which has been driven by lower interest rates in 2023, will likely be sustained by higher earnings in 2023, as well as by the market’s current, attractive valuations.

“The VN-Index’s FY23 P/E ratio is currently 30 per cent below its average over the last five years, and more than 10 per cent below that of Việt Nam’s regional peers.”

Bizhub

|